Author Shankhadeep Mukherjee

Senior Analyst and Team Leader View profile

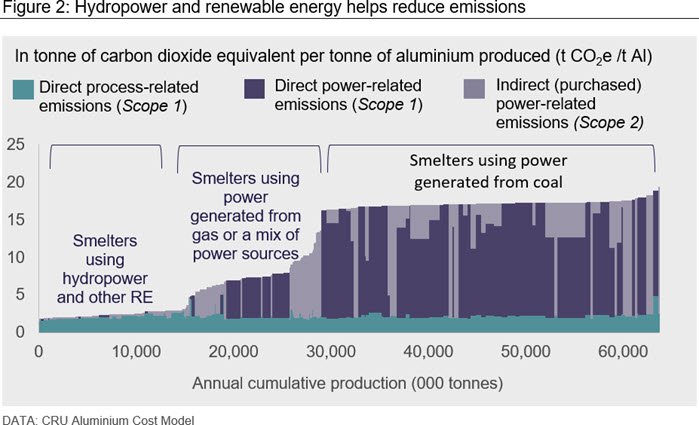

Data from CRU’s Emissions Analysis Tool shows the average intensity of CO2 emissions from Indian aluminium production is 48% higher than the global average. This is unsurprising as a significant proportion of India’s power production is coal-based.

Indeed, India’s environmental and developmental context is visible in the country’s power mix. For example, hydropower, which globally reduces carbon emissions in aluminium production, is a power source which brings its own share of problems in India. And while India does not have a carbon tax as defined in the rest of the world, there are other ways in which India does tax carbon in coal.

Indian aluminium producers can reduce their emissions, but the approach may be very different to other parts of the world. In this Insight, CRU explores the challenges and seeks to answer some of the most pressing questions.

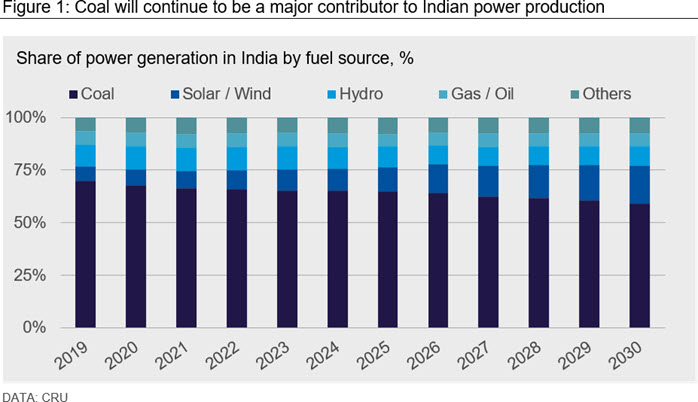

Indian power generation growth will be primarily coal-based

The growth in power generation in India is expected to be primarily driven by coal. While there is competition expected to come from renewables – particularly from solar and wind – the share of coal is expected to remain high. Though the share of power from coal is expected to reduce only to 59% by 2030 (compared to 70% in 2019), actual power production from coal is expected to increase from 1,166 TWhr in 2019 to 1,492 TWhr in 2030.

When we see Scope 1 and Scope 2 emissions in aluminium from CRU’s Emissions Analysis Tool (figure 2), we see that emissions from power generation used in aluminium is the most significant source of aluminium carbon emissions. Elsewhere, carbon emissions have been low where hydropower is available for smelting.

Hydropower generation is independent of market variations and provides relatively constant power tariffs, making it an attractive power source for smelters. However, generation capacity can vary largely with local meteorological conditions, like with other renewable energies. Hydropower may also provide significant cost advantages. For example, smelters in Canada have the lowest power cost partly due to Rio Tinto’s six smelters which benefit from the world’s cheapest electricity rates from hydropower plants with long-term amortised capital charges.

Hydro will not be an important share of India’s power supply

As figure 1 shows, the share of Indian power production from hydro is expected to remain at 10% over the medium term. The current installed capacity for hydro is very low and few new projects are under construction. This is because, in India, expanding hydropower generation would bring with it its own challenges.

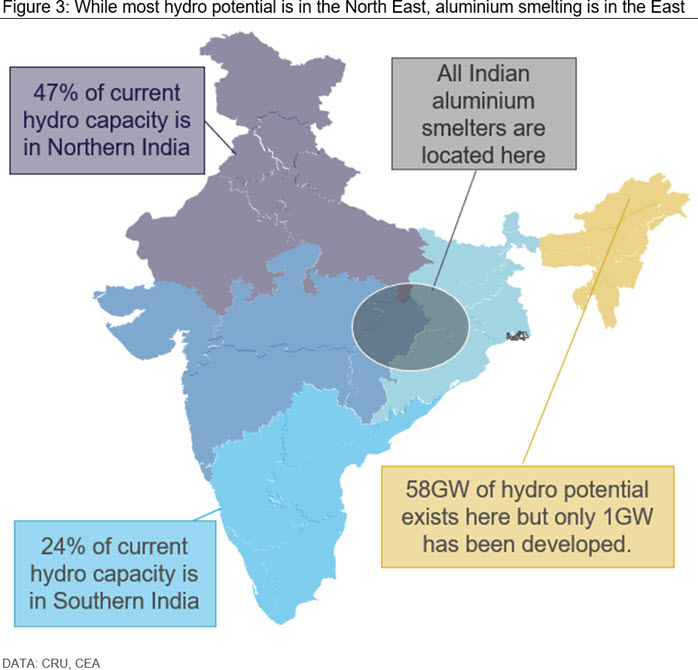

While the hydropower potential for India is around 145GW, only 28% of this capacity has been developed. Almost all current capacity is government-owned (93% of installed capacity). Nearly half of the present installed capacity (40GW) is in Northern India (19GW) and almost 65% of the total hydro potential (94GW) is yet to be developed and not under construction.

As far as potential hydro projects in India are concerned, they are based on the Brahmaputra river route which flows from China into the North Indian state of Arunachal Pradesh. However, since 1962, this area has been mired in border disputes between the two countries. There are also occasional insurgent-related issues in the region which can potentially disrupt project executions and operations. This makes the region fraught with significant geo-political risks, making it unattractive for private players in India (see figure 3).

For this reason, we do not expect hydropower generation to become an important share of India power supply. If Indian power emission intensity in metal production is to be reduced, we think it must be through other changes, and on incentives to do so. The other important point for investors to understand is how CO2 emissions costs are reflected in Indian power.

How is coal taxed in India?

While there is no separate ‘carbon tax’ on power production in India, there are a couple of ways where the cost of carbon is introduced in the cost of thermal power production.

Clean energy cess: Purchase of coal in India (including imported coal) as well as coal mined by captive producers attracts a cess which is used to fund the development of cleaner power projects in India. When introduced this was at INR50 /t of coal now it is at INR400 /t of coal. Any user of coal (thermal power plants or captive power plants) needs to pay this price over and above the notified prices of Coal India Limited along with other royalties. This is included in the cost of coal procurement in our cost models. With India switching over to a uniform goods and service tax regime from July 2017, this is now known as the compensation cess.

Renewable purchase obligation (RPO): Each state specifies some obligated entities who need to procure part of their power requirement in the form of renewable power – and this is split by solar power and non-solar power. This percentage is specified for the year the captive plant was established. In the state of Odisha, where most of Indian aluminium smelters are based, captive power plants are designated as obligated entities. There are two ways a company in India can meet RPO levels:

a. Produce their own renewable power

b. Procure renewable energy certificates (REC) on the Indian Energy Exchange

How are Indian aluminium producers handling this?

The source of power is a complex issue that the aluminium industry faces in general: smelters cannot shift power source easily. In India, this is even more complicated. Globally, 41 smelters produce aluminium from 100% hydropower. However, only nine of them have their own hydro production units. In fact, of the 180 smelters in CRU’s Aluminium Cost Model, 107 smelters operate on 100% purchased power.

The situation in India is starkly different. All three aluminium producers in India have captive power plants which can meet 100% of their power requirements, though a certain portion of grid purchase is necessary to meet RPO obligations (alongside purchase of REC). Along with captive power plants, all three primary producers also have access to captive coal sources as well as assured coal supply in the form of supply agreements with Coal India Limited, though the extent of assurance is varied by company.

In fact, as we write this insight, coal block auctions for commercial purposes are underway in India and both Hindalco and Vedanta have won coal blocks in these auctions. As these blocks are auctioned for commercial purposes without any end-use restrictions, both the producers will get additional flexibility in sourcing coal for their captive power plants. NALCO already has 100% captive / assured coal supply.

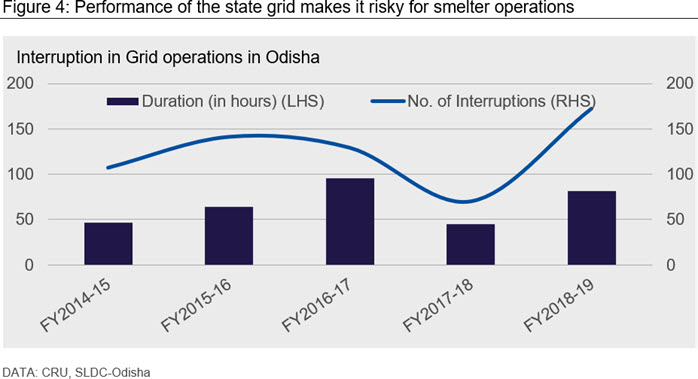

It might also be worth noting that the Indian aluminium producers could reduce their emissions by around 20% if they sourced electricity from the grid (comparable to the 2020 mix shown in figure 1), but that would result in an increase in power costs of three to four times and expose the smelters to the instability of the grid, which is an unacceptable compromise. The chart below shows the performance of the grid in the state of Odisha over the last few years.

Chart

However, producers in India need to pay both the clean energy cess as well as comply with RPO obligations as explained above. Along with paying the charges, all three producers have invested in renewable sources of power. NALCO has 198.4MW of installed wind capacity and is in the process of expanding this further by an additional 25.5MW.

Hindalco’s current renewable power generation capacity stands at 45.2MW and the company intends to expand this by another 100MW by adding a solar power plant. In March 2020, just before the lockdown in India, Vedanta floated a tender inviting interest from parties for developing 100MW solar power plant beside their Aluminium smelter at Jharsuguda.

Alongside investments in renewable power, Indian producers are also investing in recycling facilities which also help reduce emissions as well as undertake regular internal projects to reduce power consumption. In 2018, Hindalco signed a Memorandum of Understanding with the State of Gujarat to invest in 300,000 t/y scrap recycling facility (read here).

During FY2019-20, NALCO utilised graphitised cathode block in their pot line and achieved the lowest power consumption (13.367Mwh /t) in smelting operations since they started operations. Vedanta also undertook similar process which resulting in power savings for the company. The renewable power projects of Hindalco helped reduce CO2 emissions by 0.25Mn tonnes during this period.

Explore this topic with CRU

Author Shankhadeep Mukherjee

Senior Analyst and Team Leader View profileThe Latest from CRU

Singapore Commodities Briefing May 2024

We are delighted to invite you to the CRU Singapore Commodities Briefing, a regular event where industry leaders, analysts, and consultants come together to share their...