Author Anthony Everiss

Senior Analyst View profile

What becomes clear is that in all markets the CPC price has the greatest likelihood to move higher given historical pricing, whilst the tighter CTP marketplace has diverged over time as a percentage of LME and SHFE, and remains at higher levels over a multi-year analysis. Whilst the relationship between carbon and aluminium has never been as correlated as alumina, for obvious reasons, including that the supply of the raw materials for an anode’s carbon products are derived from the oil and steel industry, there is some rationale here for seeing CPC prices move higher due to stronger aluminium pricing.

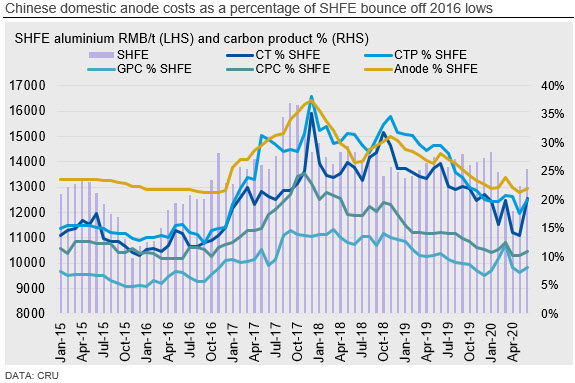

For most of 2015, anode prices in China were approximately 24% of SHFE prices, moving to 21% by 2016 before rallying to a high of 37% by the end of 2017. By the start of 2019, the anode price had started to drift below 30% of SHFE, and has now tracked back to 22%, having a brief increase in March 2020 to 24%.

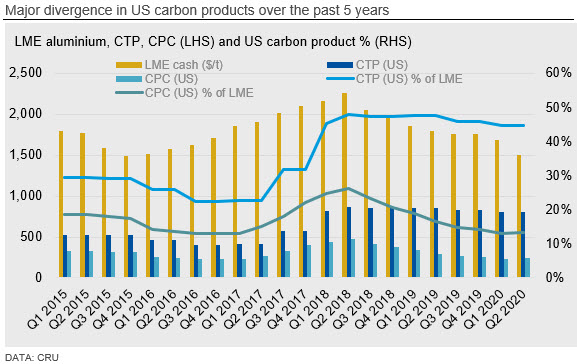

In North America, we note that CTP prices rose from less than 30% of the LME in 2015-16 to now trade in a range above 45% since 2018. CPC however has dropped from 18% in 2015 to 13% currently, having risen to 26% in Q2 2018.

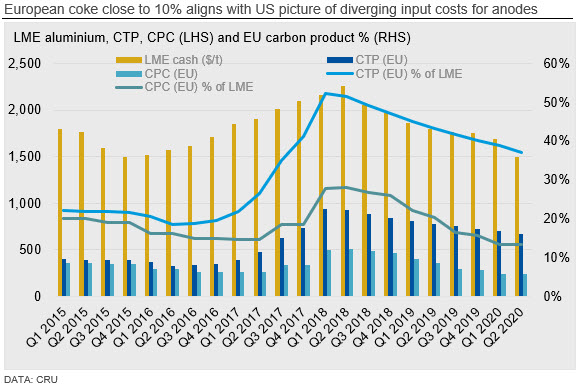

A similar pattern has played out in Europe with a divergence in CTP and CPC percentages of LME. However,CTP has fallen from a high of 52% in 2Q18 to sub 40% in 2Q20 due to lower CT pricing. CPC was 20% of the LME price in 2015, rising to 28% in 2018 before moving to 13% in 2020, in line with other regional pricing.

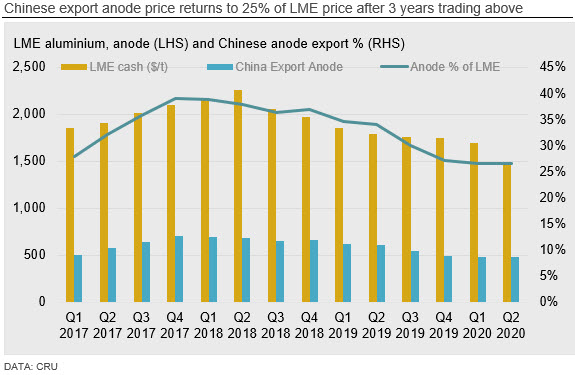

Chinese anode export prices have travelled from 25% of the LME aluminium price in 2017 to 40% by the end of that year, before steadily returning to 25% by 4Q19, where they have remained and are only expected to see a small rise over the coming 18 months.

Learn more in our recent webinar

Webinar: CRU Aluminium Q&A Session

Date/time: 26 August (recorded)

Topic: Raw materials outlook

To learn more about our latest aluminium raw materials outlook, request access to the recording of our subscriber-only Aluminium Q&A Session. The 30-minute webinar features Justin Hughes and Julia Du alongside weekly Q&A hosts Doug Hilderhoff and Greg Wittbecker. If you would like to request the recording or have additional questions, please get in touch.

Learn more about this insight

Author Anthony Everiss

Senior Analyst View profileThe Latest from CRU

Singapore Commodities Briefing May 2024

We are delighted to invite you to the CRU Singapore Commodities Briefing, a regular event where industry leaders, analysts, and consultants come together to share their...