Capacity overshooting demand

China’s booming lithium-ion battery cell industry is overshooting demand, which will lead to industry consolidation. Primary research from CRU’s battery team in recent site visits illustrates the context and scale of the issue.

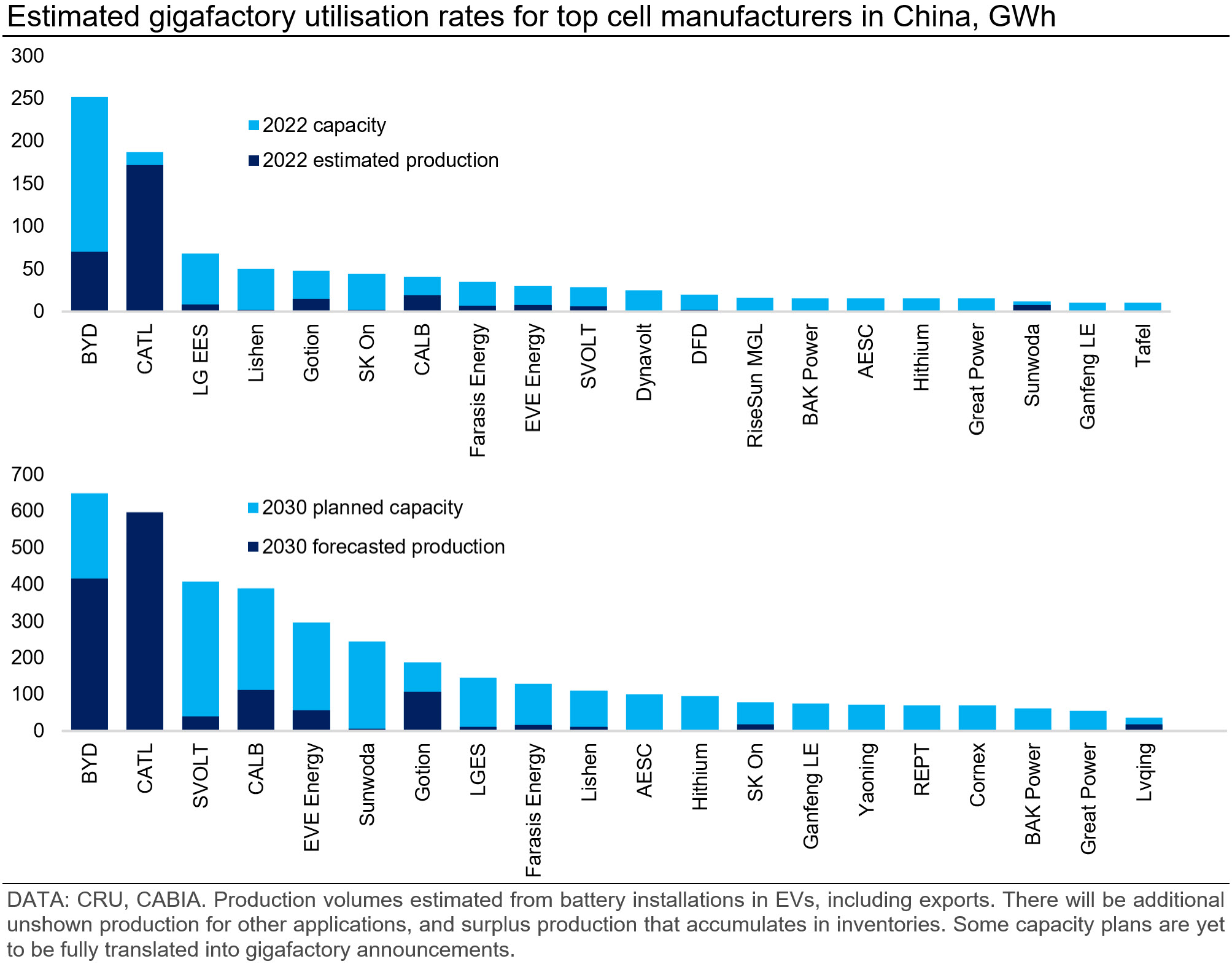

Gigafactory average utilisation rates were 45% in 2022 and have dropped further in the first half of 2023. Such numbers would have serious implications for any battery gigafactory outside of China where generally 75-85% utilisation is considered to be the point of profit.

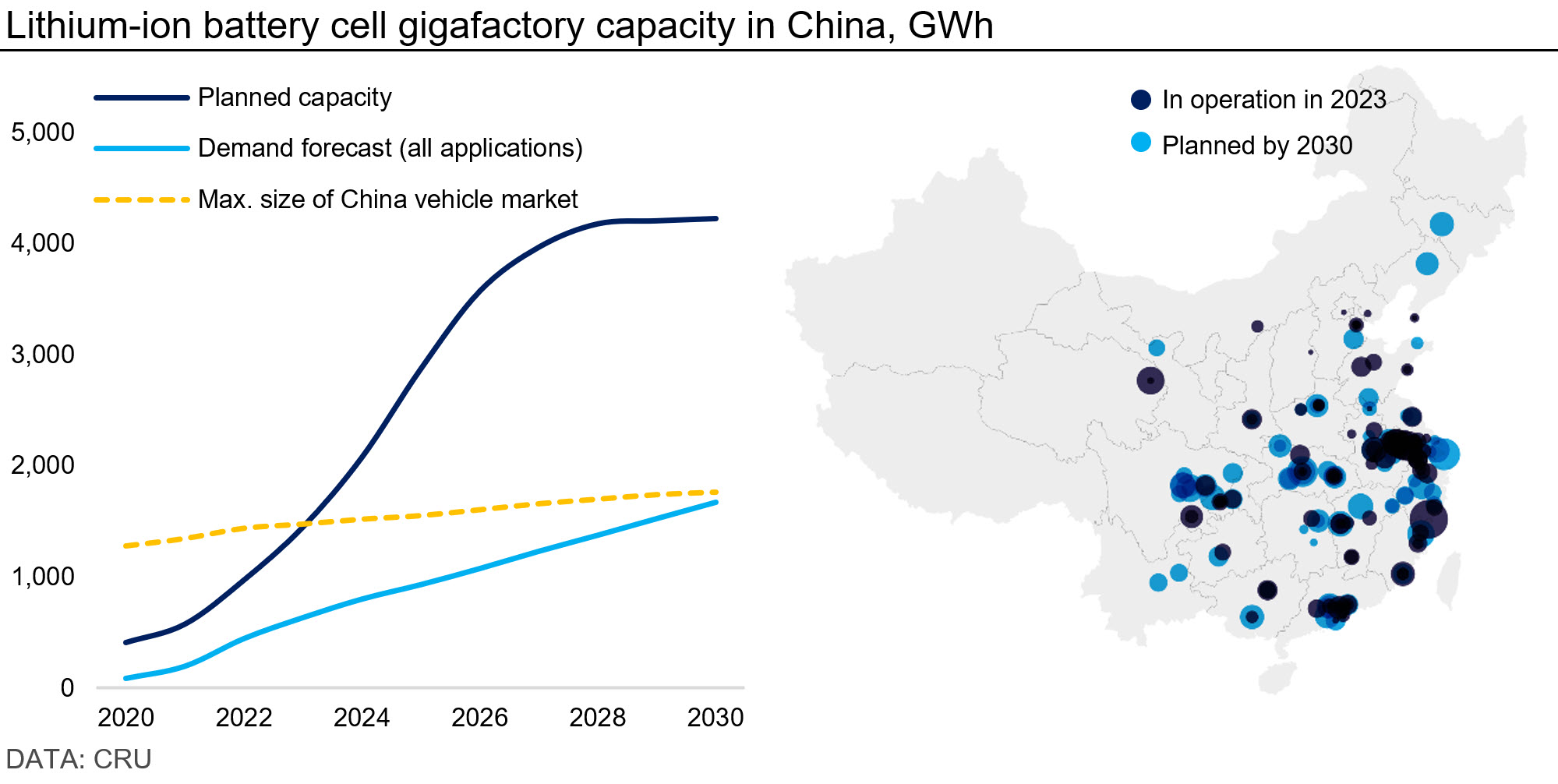

Despite the low utilisation rates, China’s gigafactory capacity pipeline has swollen to an ambitious 4,200 GWh by 2030 and new announcements continue to be made on a weekly basis. To put this in context, this is twice the GWh required if the entire China vehicle fleet were to be converted to battery-electric vehicles.

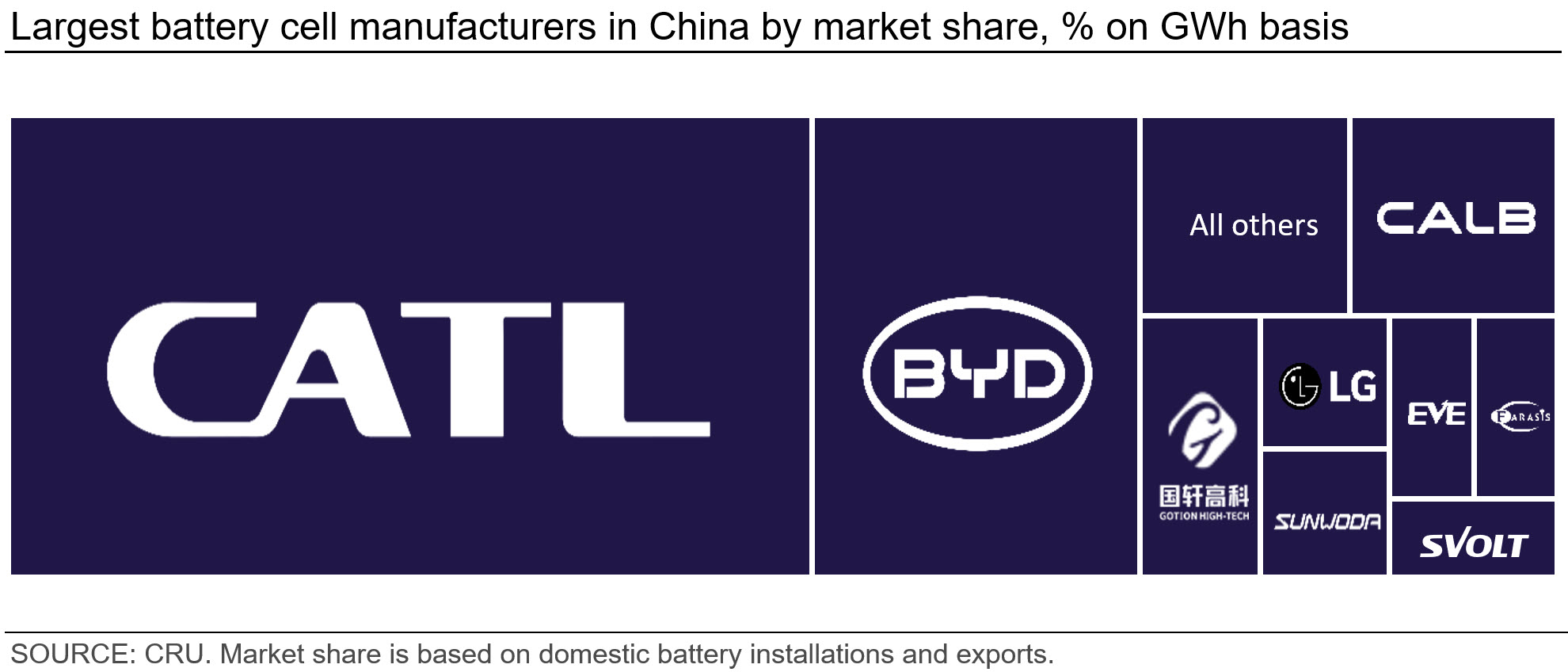

A dramatic influx of investment by both new and incumbent manufacturers has led to an increasingly crowded battery market in China. However, the Chinese market can be characterised as a near-oligopoly, where CATL and BYD hold a colossal 73% market share.

Such a ‘gold rush’ is recurrently witnessed in other industries in China where there is money to be made from private enterprise with government support. It has been seen elsewhere in the battery value chain and eventually led to cycles of consolidation – notably in the new energy vehicle (NEV) market, and is currently unfolding in LFP cathode production.

Conflicting narratives

Yet, many of these companies remain unconcerned and are prepared to take on much more risk than Western investors, especially given they have access to cheap capital and those investments have been de-risked by government support. They also weigh in the opportunity cost of not making investments, as opposed to the Western notion of prioritising a quick return on capital.

In some cases, the overall cost of producing and storing batteries has been less than the cost of idling the plant. This has led to a gradual accumulation of inventory.

Testimonies from some manufacturers admit to an intention of dialling back future investments, instead focusing on improving utilisation of existing plants. Yet, investments and announcements continue to be made by the same organisations.

What happens next?

One might think that Chinese manufacturers will seek to offload their burgeoning inventories into export markets, but this will be challenging for several reasons:

- There are already strong anti-dumping regulations in the major battery-consuming regions;

- It remains expensive to import EV batteries across regions;

- Production capacity in the rest of the world is growing;

- EV batteries are not a fungible commodity. OEMs cannot simply use a battery that has not been designed into their vehicles

The more likely scenario is one of consolidation. At some point, the lack of orders, the build-up of stock and the accumulation of capital expenditure in new facilities will lead some manufacturers to failure.

The predicted utilisation rates are an indication of the potential winners and losers. As is the case in the rest of the world, smaller manufacturers stand little chance against long-established players in an industry that requires precision and experience to withstand the high capex and tight margins.

Meanwhile, another case of overcapacity is developing in parallel – namely in LFP cathode production. This is an issue that industry stakeholders are in consensus on, and the CRU battery team will elaborate in an upcoming Insight.

Explore this topic with CRU