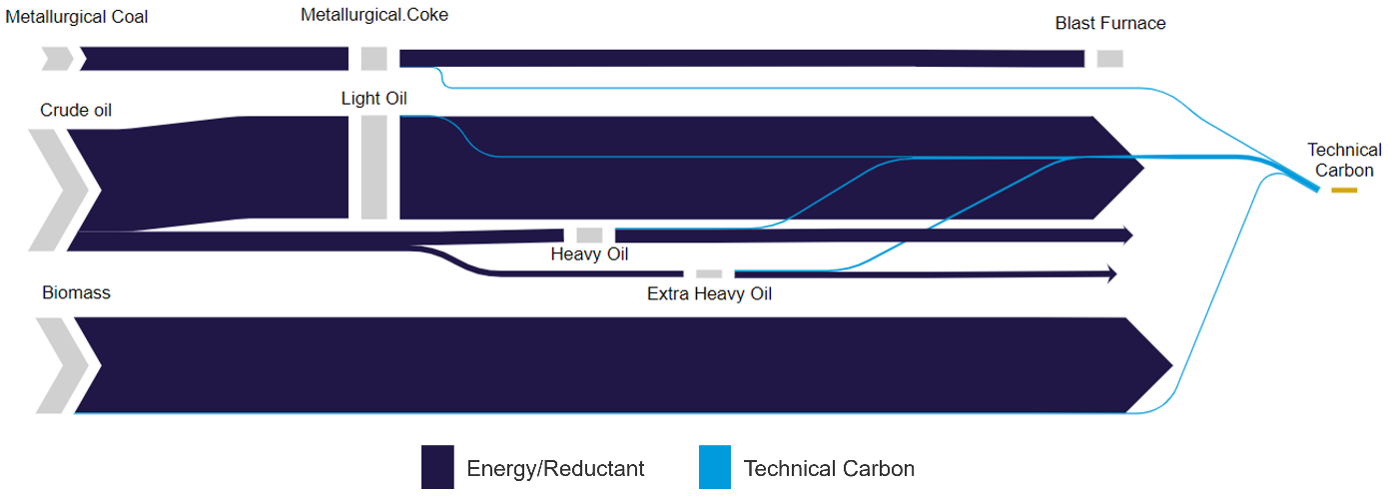

The current technical carbon market is fuelled largely by coal, oil, and gas

We have explored how decarbonisation will lead to a surge in technical carbon product demand, but how can supply support such a change when most technical carbon comes as a by-product of fossil fuels? Despite work to reduce the carbon footprint of fossil fuels, these efforts will not save technical carbon supply if oil demand declines significantly from current levels, or if coal is eliminated from its role in electricity generation.

To meet this pending supply gap, new feedstocks are needed, with much feasibility research underway investigating different carbon feedstocks, including the use of biomass and waste.

Today, the majority of the technical carbon market, in both intermediary and end-use forms, is supplied from oil and coal. Below, we can see the flows of carbon from current feedstocks.

Though far from linear, if climate goals are to be achieved, we can expect a phasing-down in utilisation of existing primary coal, oil and, to a lesser degree, gas capacity by 2050. There will be some capacity turnover, with mega oil refinery projects replacing smaller oil refineries. To explore the impact of this capacity phase down, we look specifically at oil next.

Developments are well under way in the oil industry

In oil production, there is not a straightforward barrel of oil to tonne of technical carbon ratio. Instead, we are confronted with a complex series of relationships from the well, through the refineries and their integrated delayed coking units, to the processors and users of the resulting coke products.

In a high-level simplification:

- The refining of crudes produces bottom of the barrel residuals, which can be converted into coke or blended with diesel to make heavy fuel oil, amongst other uses. The coke is a by-product, and these units are run to maximise conversion to other higher value liquid products and petrochemicals.

- The form of technical carbon necessary for use in aluminium anodes, electrodes, etc., comes from calcined pet coke (CPC). CPC comes from green pet coke (GPC) when anode quality coke is produced, as separate from fuel grade.

- The ability to produce each quality is primarily driven by the type of crude being refined at the particular refinery, with low sulphur and metals content (especially vanadium, nickel, and iron) needed for anode coke. Heavier and sourer (sulphurous) crudes are better suited to the production of fuel grade, with lighter and sweeter crudes being better suited to anode grade.

According to modelling done by CRU Consulting, a large percentage of the anode coke comes from smaller refineries, many of which are in China. These refineries are seen as the most likely to be shut down due to lower efficiency and competition from new large projects likely to come online in the coming years in China, the Middle East and elsewhere. The changing capacity mix of oil production, as well as changes to the heavy sour/light sweet mix, alongside local regulations, will drive changes in coke production volumes and the share of volume by coke type.

In our scenarios of future oil demand in 2050, we have encountered some insights:

- Smaller oil refineries will exit the market, taking their anode coking capacity offline, either with loss of demand or replacement by new projects.

- Increases in alternative maritime shipping fuels will eventually put pressure on the HFO market. This will limit ability for excess tonnes of residuals to be sent here.

- In modest growth and flat scenarios for oil production – with the above holding true still – an increase in global availability of bottom of the barrel residuals will result. Consistently high prices will incentivise existing and new refineries to add new DCU capacity

Ultimately, installing more delayed coking units will not be able to fully off-set the permanent loss of refining capacity we see in the more extreme scenarios. When this occurs, technical carbon will still be needed, and so other production routes will be explored to replace fossil fuel derived from technical carbon.

Options exist to replace fossil fuels, but there are no silver bullets

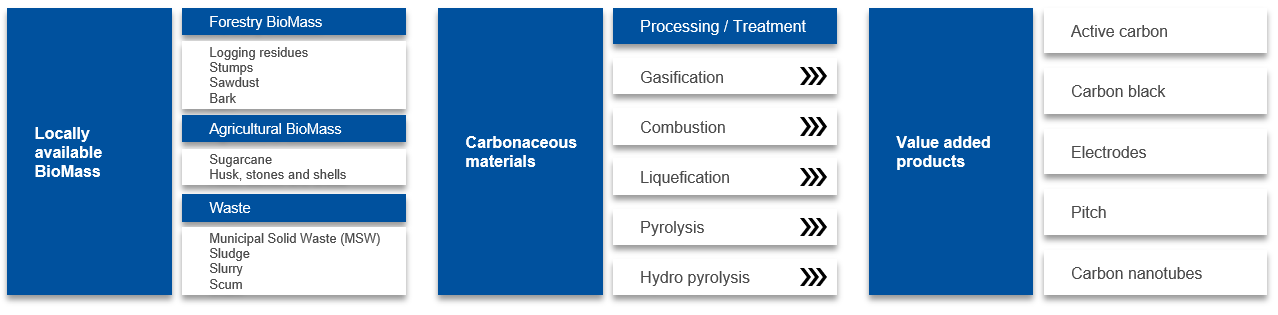

Developments in the renewable supply space have been aplenty in recent years, with biomass and waste valorisation gaining increasing academic interest. These could be attractive, incorporating elements of circularity, sustainability, and feedstock alternatives which will help meet rapidly growing demand for technical carbon.

Biomass, both plant and animal resources, be it forestry, aquatic, agricultural and organic waste, including municipal solid waste (MSW), sludge, slurry, and scum, are underutilised or undervalued today in the technical carbon space. Currently, biomass is the primary feedstock for activated carbon, but more carbon may be needed from this feedstock. Primarily in pilot phases, there is growing evidence indicating advantageous use of biomass and waste into other products like pitch, electrodes, reductants, and carbon black as shown in the diagram below.

Projects in North America, Europe and elsewhere are developing large-scale biomass processing plants, with many attached to pyrolysis plants to create bio-based products and reduce logistic costs. CRU estimates that supply of technical carbon from biomass or waste sources could reach annual growth of 3-4%, driven by:

- Decarbonisation policy

- Carbon credits

- Profits from increased valorisation

However, the route to commercial supply of biomass in particular features unique complexity. At CRU, we understand the core risks to commercialisation for suppliers in this industry, including the regional variance of biomass availability, the impacts from weather, crop yields and other factors, which lead to increased price volatility, as well as the higher variability of biomass contents relative to crude oil or coal types.

A vastly different picture

Insecurities surrounding availability of feedstock will change the technical carbon industry. Decarbonisation efforts require the industry to adapt traditional feedstock processes, alongside a willingness to investigate novel feedstocks.

Our next Insight will discuss the emerging supply gap, the possible solutions, and the implications for the technical carbon industry as a whole.

Explore this topic with CRU