Author Chris Asgill

Head of Steel View profile

This Insight is the fourth in a series of five that look at China’s capacity reduction programme and its key implications. In this Insight, we examine the impact of improved Chinese capacity utilisation on EAF production elsewhere in the world, particularly South East Asia, and on scrap market dynamics and prices. We find that, given a stronger steel price environment and lower availability of both finished and semi-finished steel in China, EAF-based production elsewhere is higher. Furthermore, higher billet prices and stronger scrap demand are supportive of higher scrap prices. Margins for EAF-based producers will decline from current levels, but not to the lows of a few years back.

Better times to remain for EAF producers in Asia

CRU forecasts ongoing increases in Chinese crude steel capacity utilisation as spare capacity is cut further. Our domestic steel price forecasts have been upgraded, and with them, expectations of industry profitability. Likewise, our outlook for Chinese steel export volumes, both finished and semi-finished, have been reduced.

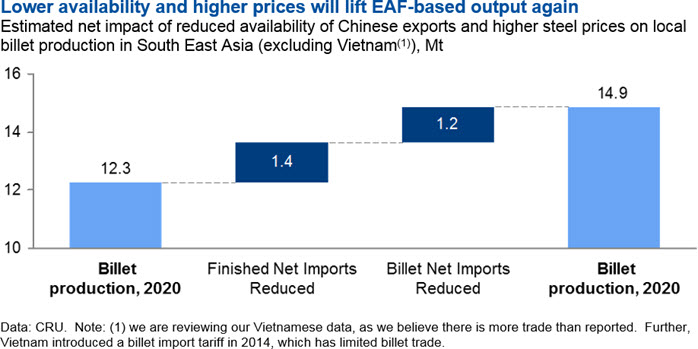

Lower availability and higher prices of billet are expected to lift EAF-based steel output elsewhere as steel producers that had, in recent years, reduced primary steel output in favour of importing lower cost billet, will be more able to produce. Scrap and billet prices represent an arbitrage opportunity for EAF-based steelmakers, something that has played out strongly since 2014. Higher finished steel and billet prices will lift scrap demand and prices as EAF-based output increase. Because scrap prices are expected to rise in line with steel prices, and domestic premiums are unlikely to rise, margins for EAF-based production are not expected to lift substantially because of higher scrap use. That said, the spread between finished steel and billet prices is expected to remain in place, which will support margins, but at a slightly lower level than in this past year. Note: for simplicity was have excluded any potential impact from a shortage graphite electrodes and higher conversion costs in this analysis; please contact us for a recent article on this topic if of interest.

Margins to remain higher, just below levels in 2017

- Higher steelmaking utilisation in China will limit steel available for export and provide support for international steel prices. This will further support higher EAF-based steel output in South East Asia, which had been reduced due to stronger finished steel and billet imports.

- Stronger EAF-based output in South East Asia will lift scrap demand and imports. However, the region is not large enough to tilt the global scrap balance. That said, a similar effect in Turkey and other major EAF-producing countries will support scrap prices.

- Margins for EAF-based output are not expected to rise substantially due to higher scrap prices and no real increase in domestic premiums. That said, a spread will remain between finished steel and billet prices, holding up margins compared to a few years back. Though, this will be at a lower level than seen this year.

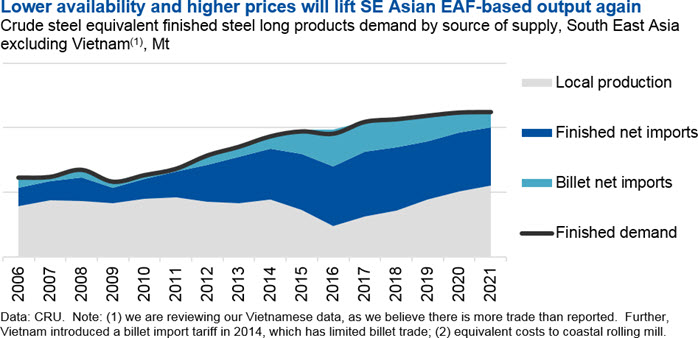

Billet imports have limited steel output growth in South East Asia

Steel long products demand in South East Asia has risen over recent years, though the pace of growth has slowed. Despite growth in consumption, EAF and billet production in the region has faltered as imports of both finished long products and billet/bloom have risen strongly. As a consequence, utilisation of regional steelmaking and capacity has been low.

Initially, buyers in the region turned to lower cost finished steel imports, as was the case in 2014 when China was pricing steel aggressively to support production via exports. Steelmakers, in an attempt to maintain their customer base, eventually turned to billet imports to support their hot rolling operations and supply finished steel to their customers. This arbitrage was possible due to a disconnect between billet and scrap prices at that time.

EAF-based steelmakers arbitrage billet and scrap prices

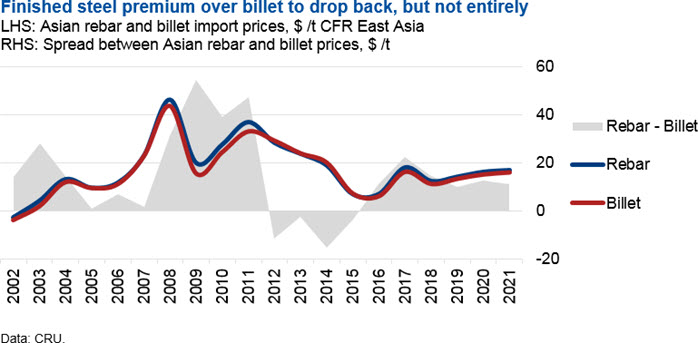

Historically, scrap and billet prices have correlated strongly on a delivered basis. This occurs as EAF-based mills in scrap-importing countries arbitrage scrap and billet prices whenever a disconnect occurs. The chart below shows the relationships between rebar, billet and scrap prices in Asia, accounting for freight and conversion costs where appropriate. When billet is comparatively cheap (i.e. the black line is above zero), imports of billet as a share of billet demand have risen strongly. The propensity for steel mills to idle facilities was also exacerbated by poor steel industry conditions in Asia throughout this period, as they not only looked to maintain sales, but contain variable costs during a period of low steel prices.

In 2017, less available and higher priced Chinese steel, coupled with low scrap prices in the first half have the year, have seen billet imports drop back substantially. This effect was greatest in Thailand and Indonesia, where imports of billet had previously risen the most. This is leading to higher EAF output in these countries, where their own billet is almost cast exclusively from EAF-produced steel. Consequently, scrap demand in the region has risen strongly: up 40% y/y to August in Thailand (n.b. Indonesia has only reported to April, but scrap imports are up over 105% y/y in the first four months of this year).

Lower billet availability and higher prices to remain beyond 2018

Higher utilisation of steelmaking assets in China has reduced the propensity of steel mills in the country to export steel. This, coupled with some transient demand and supply factors, has helped support steel prices and margins this year. We do expect that the transient factors will wane, and there is evidence of this already in falling domestic and export prices in the country. We expect this will carry into 2018, before higher utilisation levels will again limit exports and drive higher steel prices.

Beyond 2018, we expect that local crude steel production will return to stronger growth. This has driven not only lower finished steel long products and billet imports, but also rising finished steel demand in the region.

Higher EAF output will lift scrap demand and imports in South East Asia

Higher EAF-based crude steel production will provide support for scrap demand. This will lift scrap imports, as South East Asia does not have enough local supply. Typically, these have been sourced from Japan, the USA, Australia. Marginal tonnages have also been imported from Brazil and more recently South Korea.

In a global context, South East Asian scrap imports are small

Aside from Vietnam, South East Asia is not in of itself a large enough source of scrap demand to tilt the balance of the scrap market. However, other countries or regions that are, such as Turkey and to a lesser extent North East Asia, have also experienced periods of high billet imports and, consequently, lower EAF crude steel output given lower steel demand. Therefore, in aggregate, we expect that the reduced presence of Chinese steel exports and higher steel prices will provide uplift for global scrap demand.

Better steel margins will remain, but at a lower level

Because steel mills in Asia arbitrage billet and scrap, prices correlate strongly. Therefore, margins will not improve substantially because scrap use rises. Consequently, there are only three other potential areas for margins to improve: higher utilisation lowering fixed costs, higher domestic premiums, or stronger international finished steel prices compared to billet prices. The first two of these are not expected to yield gains in margins, but we do expect the premium between finished steel and billet prices will remain into the forecast period, just at a lower level than in 2017. Therefore, higher utilisation in China will sustain margins in Asia and lift scrap use in the region.

Fixed costs are low on EAF, limiting gains from higher utilisation

EAF-based production is highly flexible and has low fixed costs compared to a BOF-based steel mill. Therefore, when utilisation increases or decreases there is comparatively less change in the cost per tonne of steel produced. This means that, while production levels will increase, fixed costs per tonne are unlikely to be a significant driver of higher margins.

Domestic premiums are unlikely to increase significantly

Domestic prices in importing economies are typically set on an import parity (IPP) basis. This means domestic prices are calculated using a base price of the greatest threat of import, which has historically been China in South East Asia. Premiums to this are added to account for the costs of importing this material relative to supply from a domestic producer. These costs can be direct, such as port charges, tariffs and warehousing costs. The costs can also be indirect, such as price risk due to long lead-times, working capital costs, and what might be termed a ‘domestic premium’ for goodwill ascribed to local market knowledge, customer service, etc. Each market has its own set of premiums, though heavily commoditised steel products typically only achieve small premiums for indirect costs.

Reduced availability of steel available for imports will extend lead-times to secure material, but a steel market with higher margins is also likely to be less volatile because price movements will not be subjugated entirely to movements in raw materials costs. Therefore, higher domestic premiums due to longer lead-times creating greater price risk are unlikely.

Reduced availability of steel may allow local steel producers to extend some gains for domestic supply, as end-users look to ensure security of supply. However, while material will be less available, we are not saying that a shortage exists. So, domestic premiums are not expected to rise.

Spread between finished steel and billet to remain, just at a lower level

The final avenue to higher margins for Asian producers would be for regional finished steel prices to extend or maintain gains over billet prices. While we do not expect that the premium for finished steel over billet will remain at the levels seen in 2017, we do not expect that the premium will return to the lows of 2012 to 2015. The premium is expected to drop back slightly over the forecast horizon as we expect that steel exporters will focus more on finished steel than on billet. This will restrict availability of billet compared to finished steel, tightening the spread between prices in these markets from current levels. So, margins will be higher than those of a few years back, but they are expected to be lower than in the past year.

Explore this topic with CRU

Author Chris Asgill

Head of Steel View profileThe Latest from CRU

Key takeaways from CRU’s Wire and Cable Amsterdam conference

CRU held its seventeenth consecutive Wire and Cable conference in Amsterdam, during 24–26 June 2024. Day 1 kicked off with a warm welcome to around 200 conference...